Industry Insights

2022 US Mid-Term Elections

September 2022

- Mid-Term Elections in the US are set for November 8th, with Democrats holding narrow control of Congress in addition to the Presidency

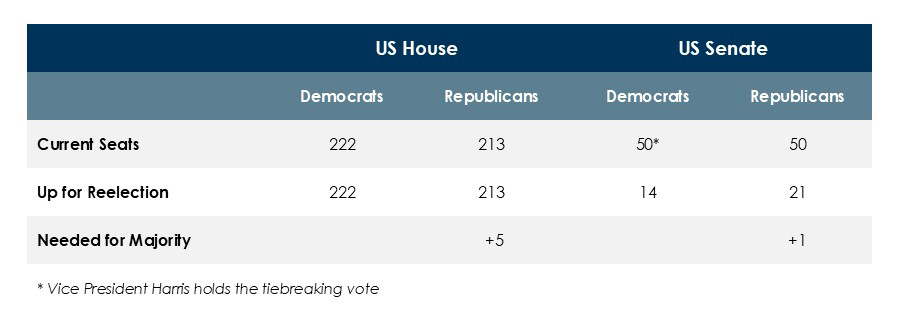

- Each of the 435 House of Representative seats and 35 of 100 Senate seats are up for re-election

- History suggests that the party of the newly elected President loses, on average, approximately 28 seats in Congress

History and Background

Mid-term elections in the US occur mid-way through a President’s term in office. All 435 seats in the House of Representatives and roughly a third of the 100 seats in the Senate are up for reelection. Additionally, the 2022 election will be the first to take place following apportionment and redistricting after the 2020 census. As a result of apportionment, six states gained seats in the US House (Oregon, Colorado, Florida, Montana, North Carolina, and Texas) and seven states lost seats (California, Illinois, Michigan, New York, Ohio, Pennsylvania, and West Virginia).

Going into the 2022 mid-term elections, the Democratic party holds narrow control of congress in addition to holding the presidency. History suggests that the President’s party will lose seats in the mid-terms, and given the Democrats’ slim margins that would almost certainly mean a split or unified Republican congress opposite Democratic President Joe Biden. From 1934 through 2018, there have been 14 mid-term elections for first time presidents. In those mid-term elections, the President’s political party lost an average of 26 House seats and two Senate seats.

.jpg "US-House-and-US-Senate-Chart-(1).jpg")

The historical tendencies are notable but there are exceptions, and the current environment will ultimately decide the election. The economy and monetary conditions tend to carry greater weight than politics in the minds of voters, and this has been shown to be most true when either was considered a headwind. That presents a difficulty for the Democratic party in the current environment, as the economic backdrop is full of negative headlines with high inflation, rising interest rates, and two consecutive quarters of negative GDP growth. However, social issues could potentially play an outsized role in this election, as some recent controversial Supreme Court decisions have served to animate portions of the electorate, particularly on the Democratic side. So while history and the economy favor a shift to a Republican congress, the situation is complex and evolving, and many races are too close to call.

What are the Potential Outcomes?

The influence of centrist members of the Democratic party has resulted in a US Congress which is already closer to gridlock over the past two years than might have been expected immediately following the 2020 election. This is best illustrated in the failure of President Biden’s full agenda in the “Build Back Better Act” to pass. This bill, initially $3.5 trillion and later scaled down to $1.7 trillion, was focused on climate change and social policy. Some aspects of Build Back Better were included in the recently passed $737 billion Inflation Reduction Act, which included investments in green energy and prescription drug reform. Elements of Build Back Better that remain unpassed include universal pre-k, expanded child tax credits, paid family leave, and further expansions to Medicare. In the less likely event that Democrats maintain control of the House and expand their power in the Senate, these remaining provisions, which represented nearly $1 trillion of spending in the original bill, would again be on the table.

Republicans taking either the House, Senate, or both, would limit major changes to spending or tax policy. There is also a risk of a budget battle resulting in a fight over the debt limit, similar to 2011. That crisis led to a brief spike in market volatility, as well as the firstever downgrade to the US Credit rating, but was ultimately resolved with minimal long-term pain. Additionally, 2021’s bipartisan Infrastructure Bill, which passed the Senate 69-30, does demonstrate the potential for limited bipartisan agreement under the current administration.

Current projections based on aggregated polling data slightly favor Democrats relative to history, with Republicans projected to win the House but Democrats projected to maintain their razor-thin advantage in the Senate.

What Matters to the Markets?

Historically, US equities generally underperform average returns in mid-term years, but outperform in the months immediately following the election. Financial markets dislike uncertainty and the lack of clear direction heading into mid-terms can be disruptive, while a more well-defined fiscal agenda following elections can improve investor sentiment. This explanation does not explain all market moves in mid-term years, however, and the prevailing market conditions are far more important to long-term market returns than temporary policy uncertainty. That said, an important takeaway from this data is that the typical mid-term result – loss of incumbent control and increased political gridlock – is not something that historically upsets financial markets.

.jpg "S-P-500-Average-Price-Return-–-1950-2021-(1).jpg")

ACG’s Position

Timing the market is difficult and positioning portfolios around an upcoming election is no different. The data is mixed regarding market performance driven by mid-term election outcomes. ACG’s position is that financial markets are currently far more focused on issues outside of US politics, such as the path of Fed tightening and the war in Ukraine, which in turn have been contributing to recent market volatility. We continue to believe investors should remain globally diversified, long-term focused, and employ risk-mitigating strategies, as appropriate.